Posted February 19, 2023 by Nick Maggiulli

A portfolio that works in economic growth and economic stagnation. A portfolio for the best of times and the worst of times. This is the idea behind the All Weather Portfolio.

The All Weather Portfolio was created by Ray Dalio and his firm Bridgewater Associates, one of the largest hedge funds in the world. Bridgewater manages over $150 billion in assets and is known for their analysis of economic cycles as one of the top global macro hedge funds on Earth.

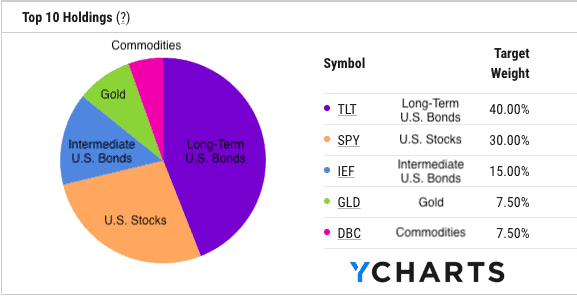

The All Weather Portfolio is an investment portfolio whose purpose is to perform well under different economic environments. Because of this mandate, the portfolio consists of 55% U.S. bonds, 30% U.S. stocks, and 15% hard assets (Gold + Commodities). [Note that this is the portfolio allocation based on Dalio’s interview with Tony Robbins in MONEY Master The Game]:

Why this particular mix of assets? Because this mixture performs well under the four economic environments highlighted by Dalio:

- Rising prices (inflation)

- Falling prices (deflation)

- Rising growth (bull markets)

- Falling growth (bear markets)

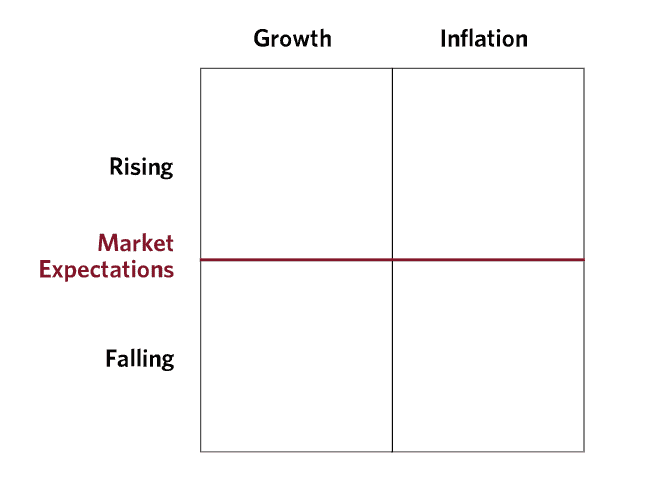

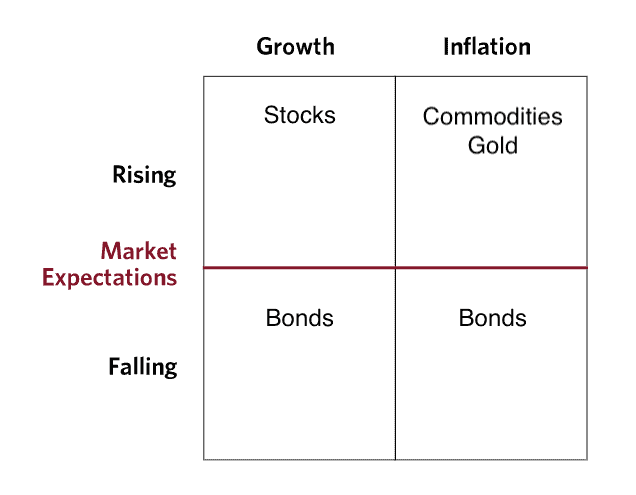

Dalio and Bridgewater have framed these four economic environments in a matrix as such:

From this matrix we can then determine which assets do best under which economic regime. For example, during periods of rising prices, commodities and gold tend to do well and during periods of falling prices, bonds tend to do well. During periods of rising growth, stocks tend to do well and during periods of falling growth, bonds tend to do wellTaking this information we can now fill in the matrix with the best performing asset under each economic environment:

{kind=link}

From here you can begin to see why the All Weather Portfolio has a higher allocation to bonds than stocks and a higher allocation to stocks than hard assets (Gold + Commodities). Since all four economic environments do not occur with the same frequency (i.e. high growth is more common than high inflation), the weightings of the assets are set to reflect this.

While this is an oversimplification of how assets react during different economic regimes, it gets at the core idea behind the All Weather Portfolio. Every asset performs differently based on what is happening in the macroeconomic environment, so your portfolio allocation should reflect this.

This might seem like an odd way to invest, but understanding the history of the All Weather Portfolio provides more clarity.

How Did the All Weather Portfolio Start?

The full story behind the All Weather Portfolio is nearly three decades in the making. After founding Bridgewater in 1975, Ray Dalio wanted to understand how assets performed following economic surprises. Since asset prices are determined by market participants’ collective expectations about the future, the only thing that can cause a major shift in assets prices is something unexpected (i.e. a surprise).

From this framework, Dalio and his colleagues set out to create a portfolio that would be indifferent to these kinds of economic surprises. As a result, in 1996 they created the All Weather fund. Initially used to house Dalio’s trust assets, Bridgewater’s All Weather fund eventually grew to $46 billion in assets by 2011.

The purpose of the fund matched Dalio’s original assertion to create a portfolio that wouldn’t react heavily to economic surprises. As Bridgewater states in The All Weather Story:

Market participants might be surprised by inflation shifts or a growth bust and All Weather would chug along, providing attractive, relatively stable returns. The strategy was and is passive; in other words, this was the best portfolio Ray and his close associates could build without any requirement to predict future conditions.

This was the key idea for Dalio and Bridgewater—find something that works no matter what the future holds.

This is a powerful concept, because, as I’ve previously discussed, no single asset class is safe now or in the future. Dalio has embraced this truth by creating a collection of assets that can provide stable returns in all economic environments. Well, that’s at least in theory. How has the All Weather Portfolio done in practice?

How Has the All Weather Portfolio Performed?

Despite the great theoretical underpinnings of the All Weather Portfolio, has it performed as expected?

Since January 2008, the All Weather Portfolio has compounded at a rate of 6% a year, which is slightly less than a traditional 60/40 (U.S. Stock/Bond) portfolio and the S&P 500:

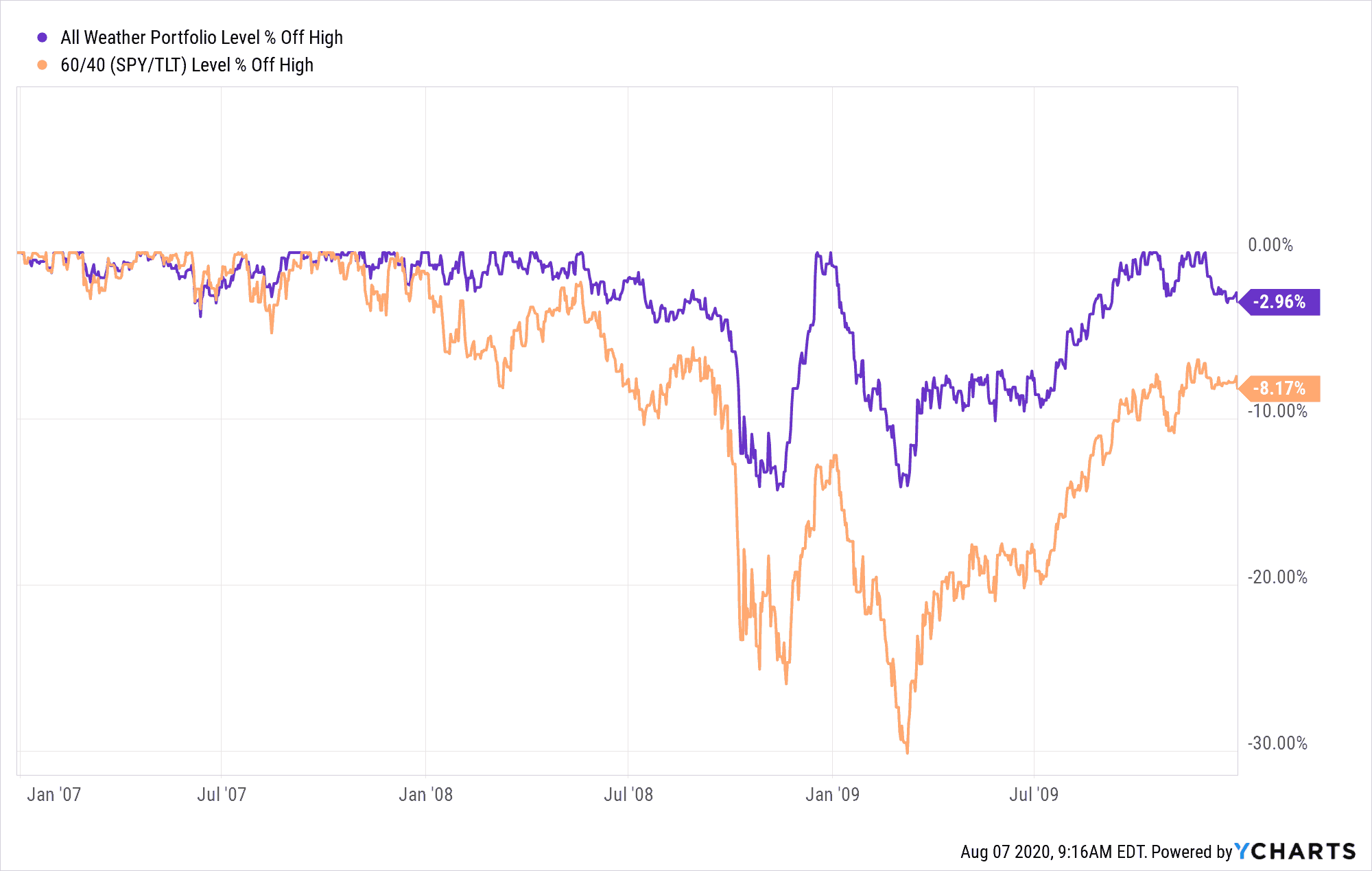

This was all while having much smaller drawdowns during most major crises:

{kind=link}

For example, during the Great Financial Crisis, the All Weather Portfolio declined less than half as much as a 60/40 (U.S. Stock/Bond) portfolio:

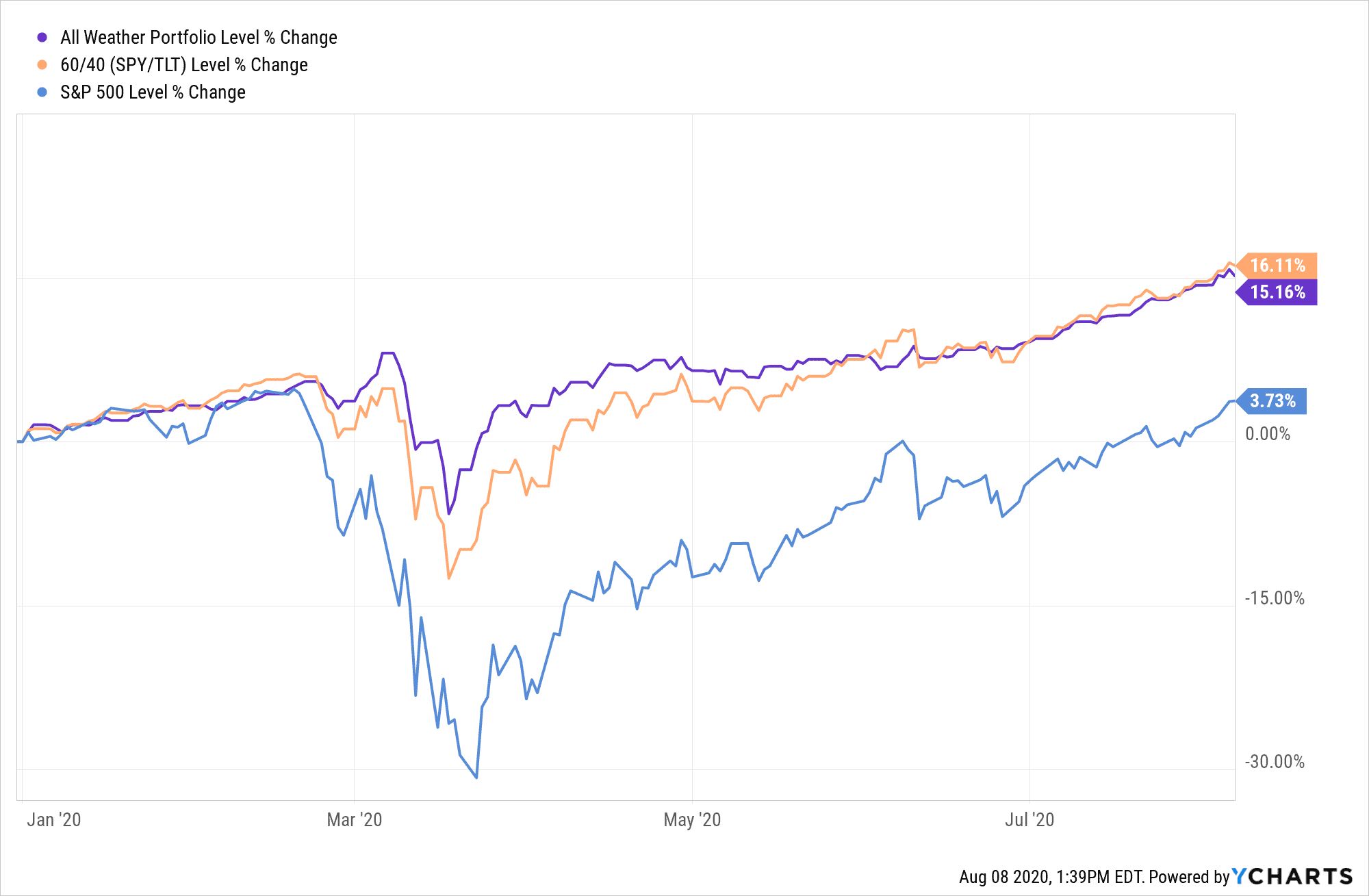

And during the COVID crash in 2020, we saw similar kinds of behavior from the All Weather Portfolio:

{kind=link}

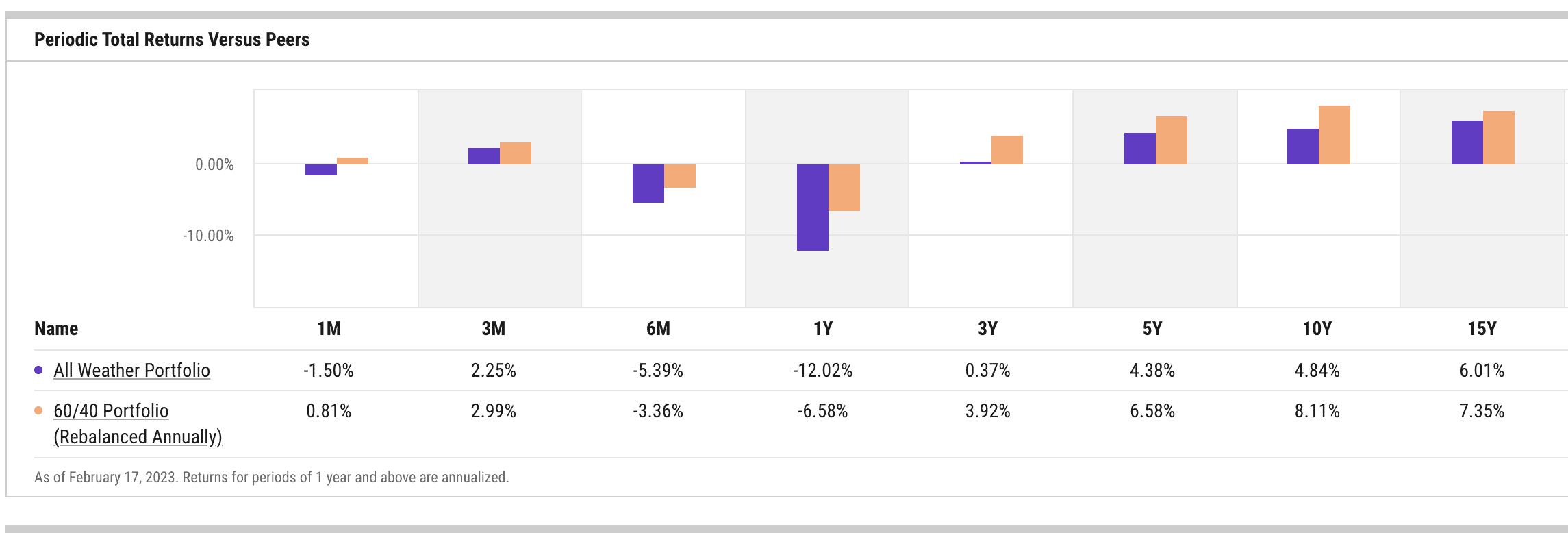

This is an impressive result, but the All Weather Portfolio has to give up some growth to obtain it. This is why the All Weather Portfolio underperformed the 60/40 portfolio over most of the last decade:

When stocks are providing high returns in a high growth environment, the All Weather Portfolio will underperform since it is only has a 30% allocation to stocks.

{kind=link}

However, in environments that are not high growth, the All Weather Portfolio is much more attractive. For example, using data going back to 1973, I found that the All Weather Portfolio outperformed the S&P 500 and the 60/40 portfolio in a high inflation environment (1970s) and a low growth environment (2000s):

{kind=link}

{kind=link}

{kind=link}

{kind=link}